5 Tax Strategies for Selling Your House or Investment Property

When selling your home, you will either have a loss or gain on the sale. If you didn’t profit above what you bought the house for initially, then you have a capital loss on the sale, which isn’t taxed. But, if you have a capital gain on the sale, you must pay capital gains taxes that will eat into the profit. Here are five strategies to help reduce or defer capital gains taxes so you can keep as much of the profit as possible.

- Timing the Sale

If you hold onto the house for over a year, you’ll pay less in taxes.

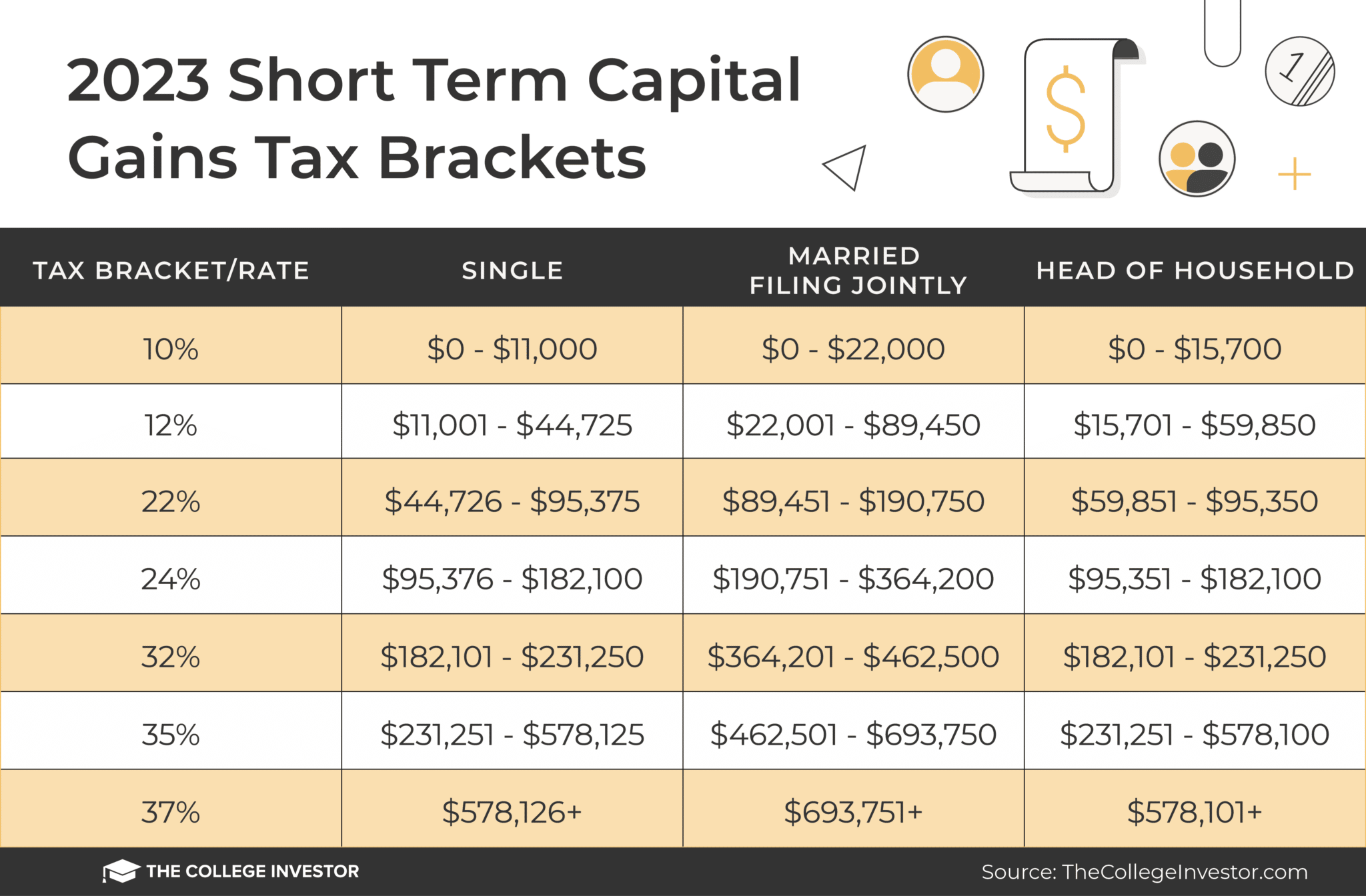

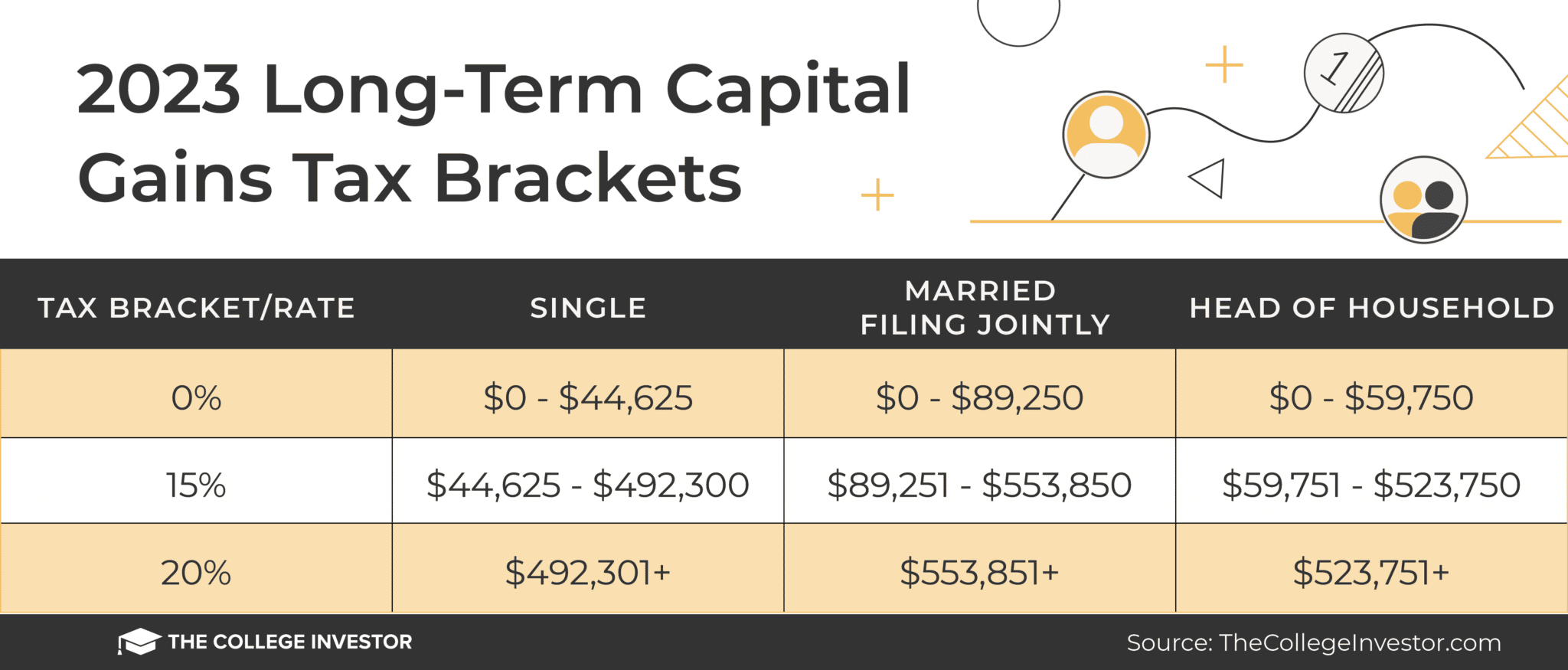

Capital gains taxes affect all your investments, including your home, stocks, bonds, or businesses. There are two types of capital gains taxes: short-term and long-term.

Short-term capital gains tax rates are what we pay on the gains on investments we sell within less than a year. These rates are the same as ordinary tax rates, the same tax rates you pay on your salary at work, which can be as high as 37%. Long-term capital gains tax applies to investments held for over a year before being sold, which can only be as high as 20%.

Therefore, if you’re debating on when it would be best to sell your home or investment property, waiting over a year to sell can dramatically reduce your tax bill.

- Tax Loss Harvesting

You can reduce capital gain taxes on the sale of your house by having losses in other investments.

When calculating the taxes you pay on capital gains, you must first add all the profits and losses on all your investments from the year. It’s important to remember that all investments have capital gains and losses, so you could use completely different investments in your total annual capital gain calculation. However, you can only subtract long-term capital losses from long-term capital gains and short-term capital losses from short-term capital gains.

For example, you had a house that you sold for a $50,000 capital gain. You also sold some stock for a $40,000 capital loss. To calculate the total capital gain/loss on the year, we must subtract the loss from the gain, leaving us with a $10,000 capital gain. We only have to apply capital gain tax rates to the $10,000 rather than the $50,000.

It’s important to note that if we have an overall capital loss on the year, we can carry that forward and subtract it from future years’ capital gains.

- Primary Residence Exclusion

If the property was used as your home, you may be able to cancel any capital gains taxes.

If you have lived in the house as your primary residence for at least two of the last five years before selling, you may qualify for the primary residence exclusion.

When you sell your house, the profit is what is being taxed here, not the price you sold it for. This exclusion allows you to exclude up to $250,000 (or $500,000 for married couples filing jointly) of the gain from being taxed.

So, say you’re married and bought a home for $500,000. You’ve lived there for at least two years, and you turn around and sell it for $1.25 million. Only $750,000 would be subject to capital gains tax. With this exclusion, you don’t have to pay taxes on $500,000 of the gain since you’re married and meet the requirements. You would only have to pay capital gains taxes on $250,000 rather than on the full $750,000 capital gain.

If you’ve lived in the house for two out of the past five years, you can dramatically reduce the taxes you pay on the sale.

- 1031 Exchange

If you’re selling an investment property and plan on buying another one, the 1031 exchange allows you to do the replacement without paying any capital gains taxes.

A 1031 exchange is like a tax-saving trade for real estate. If you sell a property and buy another similar one, you can delay paying taxes on your profit. It works by swapping one property for another without owing capital gains tax immediately. This helps you invest more money in a new property.

You need to meet specific criteria to qualify for the exchange. The first is that the new property needs to be a “similar property.” This definition is broad for real estate and mainly means that if you’re selling a commercial or residential property, the new one needs to be a part of the same class and be similarly valued.

The second is that you must buy the next property within 180 days after you sell your home. You must also identify the property you will buy within the first 45 days. These rules are challenging to follow because it is hard to find a similar property to buy in 45 days, making it essential to plan.

It’s crucial to understand that the capital gains tax isn’t being erased; rather, it’s being pushed off to be paid later.

- Opportunity Zones

If you want to wait to pay taxes on realized capital gains and have future tax-free investments, investing in opportunity zones may be the strategy for you.

Created under the Tax Cuts and Jobs Act of 2017, opportunity zones are poor areas offering major tax breaks for investments within them.

Investors can put their realized capital gains, like profits from stocks or real estate, into a Qualified Opportunity Fund (QOF) within 180 days of realizing the gain. By doing so, they can wait to pay capital gains taxes on the rolled-over amount until December 31, 2026, or until they sell the QOF investment, whichever occurs first. Waiting to pay taxes allows you to have more money to invest, growing your money faster.

QOFs invest in real estate, startups, existing businesses, and even infrastructure projects within designated Opportunity Zones.

Parking your cash in the QOF allows you to reduce the taxes on the gains within the fund. Holding the QOF investment for at least five years results in a 10% reduction of the capital gains tax, which increases to 15% if held for seven years. The most substantial benefit is realized when an investor has the QOF investment for at least ten years, as any capital gains generated from the appreciation of the QOF investment become entirely tax-free.

In summary

Five strategies to pay less in capital gains taxes on selling your home.

- Wait over a year to sell the house to get a better tax bracket.

- Use investment losses from the same and previous years to reduce capital gain.

- Exclude a portion of the capital gain if it’s a primary residence for two out of the last five years.

- If you replace the sale of a property with a purchase within a 180 days, defer capital gains tax to the future.

- Invest in opportunity zones to get tax breaks.

Similar Articles

Retirement Income

Retirement Planning

Economy

Government

Stock Market

{kind=link}

{kind=link}